Cash flow pressure is nothing new in agriculture. What has changed is the scale and volatility of input costs.

From fertiliser and fuel to feed and labour, farmers are being asked to commit more capital, earlier in the season, with less certainty on returns. That creates a familiar problem. High upfront costs, delayed income, and limited flexibility when conditions shift.

This challenge is becoming more pronounced as farming businesses face tighter margins, increased input dependency, and greater exposure to global supply chains. Even well-run farms with strong balance sheets can experience pressure when multiple cost increases hit at once.

Agricultural input loans are designed to address exactly that gap, helping farms secure what they need to operate without putting unnecessary strain on working capital.

What are Agricultural Input Loans?

Agricultural input loans are short-term, specialist funding facilities that allow farmers to purchase essential inputs without paying for them upfront.

They are typically structured around the farming cycle, with repayment aligned to key income events such as harvest or livestock sales.

In practical terms, they allow you to:

- Secure inputs when you need them

- Spread the cost over the season

- Match repayment to revenue timing

Rather than funding inputs out of cash reserves or stretching existing overdrafts, input loans create a dedicated facility for seasonal costs.

In many cases, they sit alongside existing bank facilities, providing a more structured and purpose-built approach to funding operational expenditure. This separation can improve financial visibility and make it easier to plan across multiple growing cycles.

The Benefits in Practice

The value of input finance becomes clearer when you look at how it operates on the ground.

Input loans can improve cash flow management by bridging the timing gap between planting and income generation. Instead of absorbing high upfront costs, farms can maintain liquidity for day-to-day operations and unexpected expenses.

This becomes particularly important during periods of uncertainty, where weather conditions, commodity prices, or supply disruptions can quickly impact both costs and income. Having access to flexible funding reduces the need for reactive decision-making.

Input loans can help protect margins in a volatile cost environment. Input costs have risen sharply in recent years, increasing by an average of 44% since 2019 according to AHDB.

While some categories have eased, volatility remains.

According to AF Group:

- Fertiliser prices have increased by nearly 11%

- Contract and hire costs are up over 6%

- Machinery, fuel and electricity have risen by almost 3%

- Retail Price Index (RPI) sits at 5.2%

At the same time, some inputs have fallen:

- Chemicals down 11.2%

- Animal feed and medicines down 7.4%

- Seed down 1.2%

This mixed picture makes timing and purchasing strategy critical. Input finance allows farmers to act when prices or availability are favourable, rather than when cash allows.

Input loans can also help to improve purchasing power and support productivity. Access to funding enables participation in early-order programmes and bulk buying opportunities, often securing better pricing and guaranteed supply.

Reliable access to inputs means farmers are less likely to compromise on quality or application rates. Over time, this supports stronger yields and more consistent output.

Input loans offer financial flexibility. Because they are separate from core borrowing facilities, they free up existing bank lines for longer-term investment such as land, infrastructure, or diversification.

They can also support better financial discipline, with clearer allocation of costs and more predictable repayment structures aligned to farm income cycles.

What can Input Loans be used for?

While primarily designed for seasonal inputs, these facilities are more flexible than the name suggests.

Common uses include:

- Seed, fertiliser and crop protection products

- Animal feed and medicines

- Fuel and energy costs

- Labour and contractor payments

- Machinery hire and short-term operational costs

More broadly, agricultural finance can also support:

- Livestock purchases

- Land acquisition or expansion

- Renewable energy projects

- Diversification into new income streams

- Property development, repairs and upgrades

- Business restructuring and recovery

This broader flexibility allows farms to respond to both planned investment and unexpected challenges, while maintaining operational continuity.

The key distinction is that input loans focus on short-term, revenue-linked costs rather than long-term capital investment.

How does it work in practice?

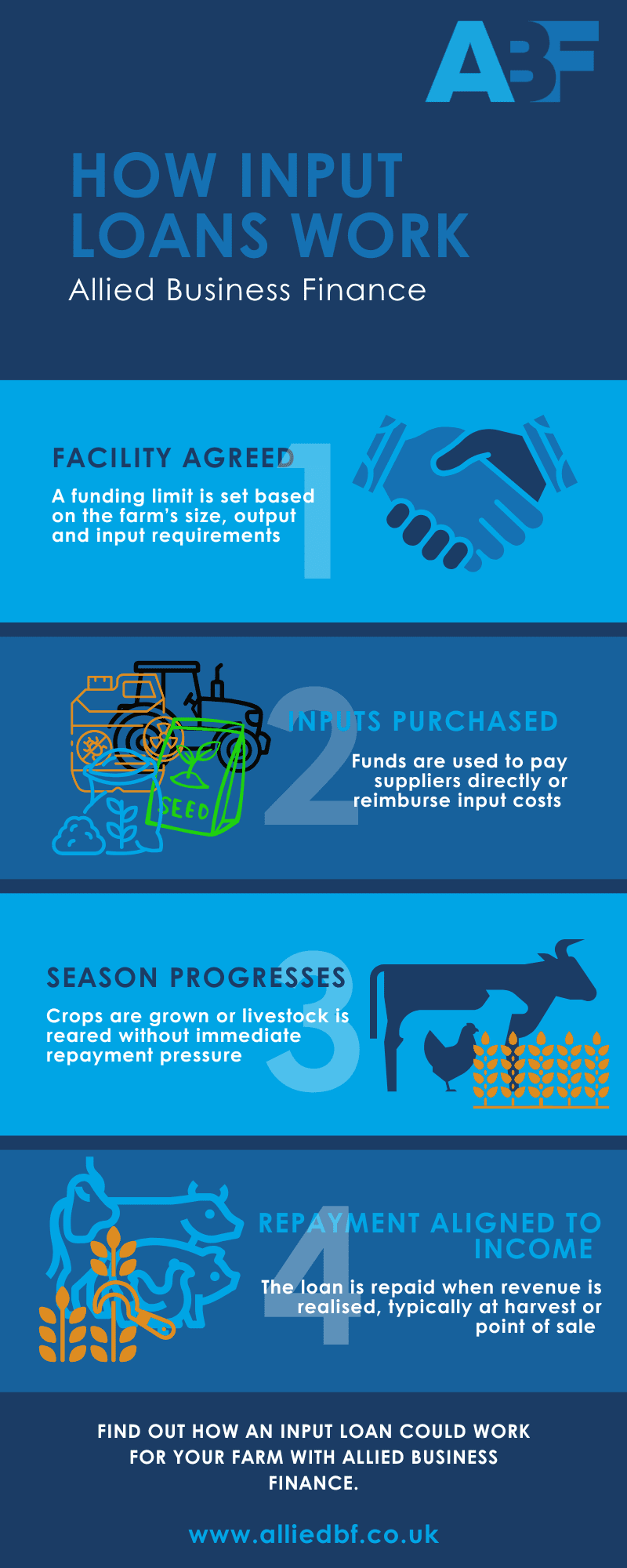

At a high level, the structure is straightforward and built around the farming cycle.

At a high level, the structure is straightforward and built around the farming cycle.

A facility is agreed with a funding limit set based on the farm’s size, output and input requirements.

Inputs are purchased using funds to pay suppliers directly or to reimburse input costs.

The season progresses with crops grown or livestock reared, but without any immediate repayment pressure.

Repayment is aligned to income, meaning the loan is repaid when revenue is realised, typically at harvest or point of sale.

This structure ensures that finance supports the natural rhythm of the business, rather than working against it.

Are input loans right for your farm?

Input loans are not a one-size-fits-all solution, but they are particularly effective where:

- Input costs are placing pressure on cash flow

- There is a clear seasonal revenue cycle

- Existing facilities are being stretched by short-term costs

- There is an opportunity to improve purchasing timing or scale

They are less about increasing borrowing, and more about structuring it correctly.

For many farms, the real benefit is improved control, with greater visibility over costs, clearer repayment planning, and the ability to act decisively when opportunities arise.

Used well, they create separation between operational spend and long-term investment, which is often where financial strain begins.

The Bottom Line

Agricultural input loans provide a practical way to manage one of the biggest challenges in modern farming: the mismatch between when costs are incurred and when income is received.

By aligning finance with the farming cycle, they:

- Reduce pressure on working capital

- Improve purchasing flexibility

- Support productivity and output

- Create headroom for longer-term investment

In a market where input costs remain unpredictable, that level of control is increasingly valuable.

What next?

If rising input costs are putting pressure on your cash flow, or your existing facilities are being stretched to cover seasonal spend, it may be time to look at a more structured approach.

At Allied Business Finance, we work with farming businesses to put dedicated input funding in place that aligns with how your operation actually runs. That means facilities built around your production cycle, your income timing, and your growth plans, not a generic lending model.

If you want a clearer view of how input finance could work for your farm, we can review your current setup and identify where a more tailored solution could improve cash flow, purchasing flexibility and overall financial control.

Get in touch to arrange a straightforward, no-obligation conversation.

Follow us on LinkedIn, Facebook, and Instagram to stay up to date with everything Allied Business Finance.